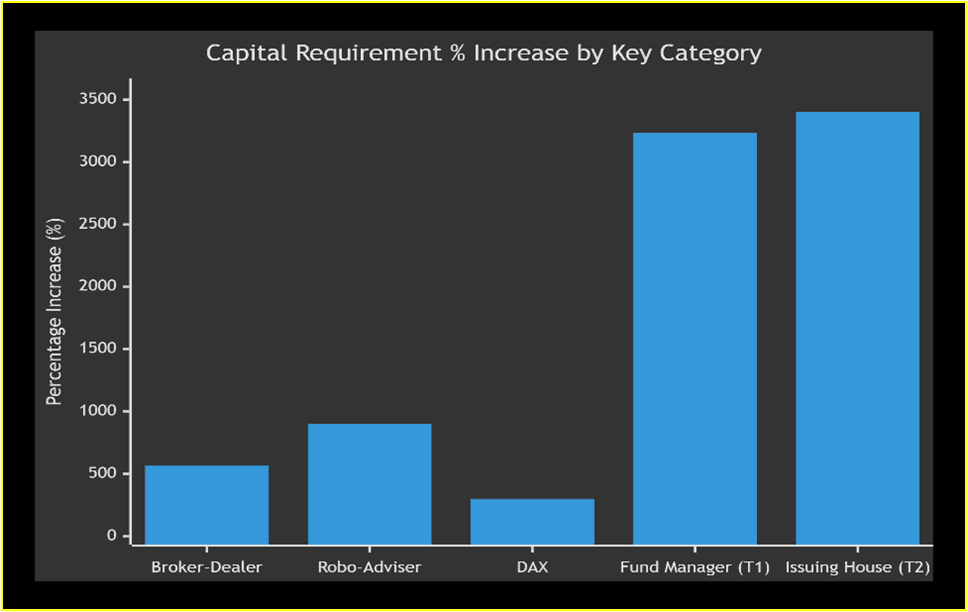

Figure 1: Bar chart showing the steep, multi-fold percentage increases in minimum capital requirements for five key categories of capital market operators. Issuing Houses (Tier 2) and Fund Managers (Tier 1) face the most significant increases, exceeding 3,200%.

Stakeholder reactions to regulatory updates typically vary– with stakeholders speaking on how they are affected. Operators may disagree with certain aspects of the reforms– due to the unplanned compliance burdens and costs. On the other hand, regulators will continue to strive towards the goals that keeps the market sophisticated and viable. For existing and new participants in Nigeria’s capital market, the following implications are worth noting:

- Consolidation and Market Restructuring

The steep increases will inevitably drive industry consolidation. Smaller operators, especially sub-brokers, individual investment advisers, and lower-tier fund managers, may seek mergers, acquisitions, or exit the market. This aligns with SEC’s objective of creating fewer, but more resilient, entities.

- Entry of New Capital and Investors

The revised thresholds may attract new domestic and foreign institutional investors seeking to acquire stakes in recapitalising firms or establish new entities, particularly in high-growth segments like digital assets and commodities.

- Risk Management and Operational Resilience

Higher capital bases will enable firms to among other benefits, withstand operational and market shocks – this in turn, makes the market attractive. It can also enable operators to invest in better technology and compliance infrastructure; and support larger and more complex transactions, especially in underwriting and fund management.

- Specialisation vs. Diversification

The tiered structure (e.g., in Fund Management and Issuing Houses) encourages specialisation. Firms must decide whether to operate in a narrow, well-capitalised niche or diversify into higher-tier categories requiring exponentially more capital.

There is notably a touch of the framework on emerging sectors like Fintech, Virtual Asset Service Providers (VASPs) & commodities. Paragraph 4 of the circular formally integrates these previously less-regulated sectors into the mainstream framework. The VASPs are clearly within the high thresholds (₦500 million to ₦2 billion), which signals precise regulatory intent. While this will improve investor confidence, it may squeeze out smaller crypto-native platforms. The FinTechs: Robo-advisers and crowdfunding intermediaries now also have defined capital bases. Noteworthy, amidst the fear that these developments may discourage start-ups, the outlook has great potential to promote stability in Nigeria’s digital finance. Also, the Commodity Market Intermediaries received significant raises, especially for warehousing operators (₦50m – ₦500m), reflecting the physical asset-backed nature and risk of this market.

4. COMPLIANCE TIMELINE & TRANSITIONAL ARRANGEMENTS: RECOMMENDATIONS

Operators must prepare for the adjustments and transition arrangements that the recapitalisation has called for. The following are worthy of note:

- Deadline for compliance is set for 30 June 2027, hence, the need to start early and act fast cannot be overemphasised.

- Entities operating in the market as a matter of first step must consequently conduct a capital adequacy gap analysis, to understand their next steps. When capital shortfall is determined and explore options: fresh equity injection, mergers, strategic divestment, or business model re-alignment. It also calls for strategic planning to decide whether to upgrade, downgrade, or consolidate operations based on the new tiers.

- SEC indicates willingness to consider case-by-case transitional arrangements upon application.[9] This makes early engagement with the Commission crucial, should any entity foresee challenges.

- The Circular underpins sanctions for non-compliance, leading to suspension or withdrawal of registration;[10] among others.

Tailored professional advisory can assist entities to turn a regulatory mandate into a competitive advantage that has the potential to attract stronger investors and attain improved market trust. Experienced capital market professionals can advise and conduct capital gap analyses, restructuring and executing compliance pathways, and formally engaging SEC for clarifications and transitional relief. Importantly, they serve essential purposes in advising and structuring capital raising arrangements and divestments.

5. CONCLUSION

Where the market becomes formidable, its viability is more likely in practical terms. Circular No. 26-1 is a transformative regulatory intervention that will reposition Nigeria’s capital market environment. While it poses significant short-term compliance challenges, it serves the long-term interests of market stability, investor protection, and sustainable growth. The recapitalisation strengthens the SEC’s ability to fulfil its ISA 2025 mandate, particularly in safeguarding investors and reducing systemic risk. Market participants must act swiftly and strategically to navigate this new regime, turning regulatory change into a competitive advantage.

Footnotes.

[1] SEC Nigeria Circular No. 26-1 (2025); Investments and Securities Act, 2025. Available at: view link

[2] Ibid, para 5.

[3] BusinessDay, ‘SEC new capital base: Capital market operators seek December 2015 deadline’ (5 November 2014) view link accessed 2 February 2026.

[4] SEC Nigeria Circular No. 26-1 (2025); Investments and Securities Act, 2025, paras 1 and 2.

[5] Others points of alignment include:

- Protection of investors (Sec. 3(2)(a) ISA): By ensuring operators have sufficient financial buffer to honour obligations.

- Maintenance of fair, orderly, and efficient markets (Sec. 3(2)(b) ISA): Through enhanced stability and reduced systemic risk.

- Reduction of systemic risk (Sec. 3(2)(c) ISA): By aligning capital with the scale and complexity of operations.

- Promotion of the development of the capital market (Sec. 3(2)(d) ISA): By providing a robust foundation for innovation, including digital assets and commodities trading.

[6] Review of Minimum Capital Requirements for Commercial, Merchant, and Non-Interest Banks in Nigeria – FRP/DIR/PUB/CIR/002/009. Available at view link

[7] SEC Nigeria Circular No. 26-1 (2025); Investments and Securities Act, 2025, para 3.

[8] SEC Nigeria Circular No. 26-1 (2025); Investments and Securities Act, 2025, para 4.

[9] The Circular No. 26-1, para 6.

[10] The Circular No. 26-1, para 5.

")

")